Inukshuk Capital Management (ICM) is a multi-asset class, high-net-worth wealth management firm. We help individuals and families achieve financial longevity by tailoring solutions that integrate their unique financial planning considerations with modern wealth management approaches designed to deliver superior returns while minimizing tax and fees.

We are pleased to share our monthly newsletter which contains information on our ETF portfolios, as well as market commentary and other relevant news.

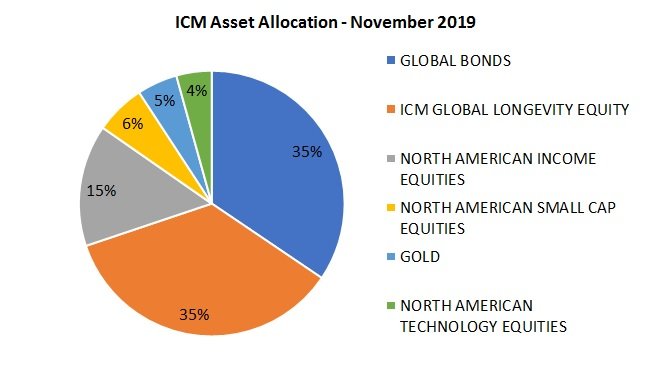

Portfolio Composition

The TSX Composite and S&P 500 indices maintained the momentum of early November and closed the month at all-time highs. In the first week of December, both markets suffered quick losses of 1.3% and 2.3% respectively but rebounded by Friday and closed very near to where they started. The gains in the MSCI Europe, Australasia and Far East (EAFE) index all occurred in the first few days of November and then chopped around to end the month up 1.1%. Emerging Markets (EM) had similar price action but only managed to close the month flat.

Our Longevity portfolio entered November with an 80% exposure to global equities. We added to these positions throughout November, and by the end of the month we were fully invested in all four markets, the S&P 500, TSX, EAFE and EM. At the close of the first week of December, three of these positions remain steady, with a slight reduction in EM due to its relative weakness.

If you would like to stay current on our measures of trend and momentum in the markets we follow, please click here.

Investment Trends

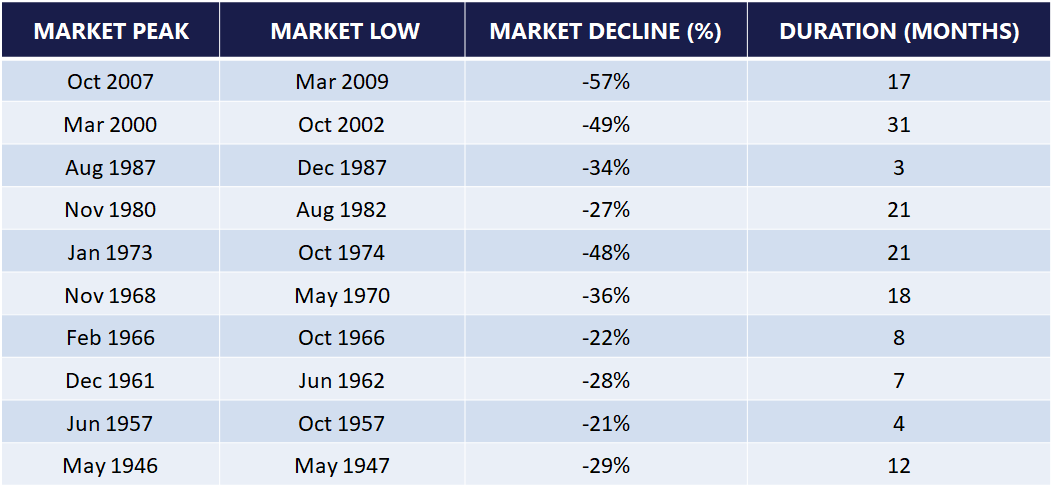

The last bear market ended in March of 2009, nearly 4000 days ago. To say that the current bull market is long in its tooth by historical standards is an understatement. Are you prepared for the next bear market? Now might be as good a time as any to begin thinking about this important question.

Read More: Are You Prepared for a Bear Market?

Historical Bear Market Declines – S&P 500

Other Markets, Central Banks and the Dollar

The most recent rate cut of 25 basis points by the Federal Reserve lowered the federal funds target to a range of 1.50 – 1.75%. The expectation of further cuts has remained stable at roughly 20% to March 2020. Looking out to the end of 2020, the odds the target range will be as low as 1.00-1.25% are around 20%. The 10-year Treasury yield moved as high as 1.97% in early November and ended the month at 1.77%.

On December 4th the Bank of Canada maintained its overnight policy target rate at a level of 1.75%, which has not changed since October 2018. The press release stated: “…trade conflicts and related uncertainty are still weighing on global economic activity, and remain the biggest source of risk…” The current odds of a 25 basis point cut by March are 10%, down from 32% in early November. The odds the overnight rate target is 25 basis points lower by December 2020 are 28%. The lowest available 5-year fixed major bank mortgage rate remains at 2.87%.

The Canadian dollar sold off versus the US dollar and closed the first week of November at 1.3275. The trading range, which has existed for more than a year, 1.3000 – 1.3600 USD/CAD, is still intact. This means a Loonie has been worth around 75 US cents since October 2018. The 3-month BA rate (BA = Banker’s Acceptance, a key rate for Canadian financial products) is 1.86% and has not moved significantly since March. The 3-month LIBOR (London Interbank Offered Rate, one of the most important USD reference rates, globally) is 1.89%. The short-term rate advantage of the US dollar has tightened slightly, but it still pays to own US versus Canadian dollars.